Table Of Content

This loan type is specifically designed for families looking to buy homes in rural areas. Similar to the FHA loan, this home loan lets lower-income families become homeowners. The loan does not require a down payment, but you will have to get private mortgage insurance. Fixed-rate loans have the same interest rate for the entire duration of the loan. That means your monthly home payment will be the same, even for long-term loans, such as 30-year fixed-rate mortgages.

How Much House Can I Afford on a $75K Salary? - Yahoo Finance

How Much House Can I Afford on a $75K Salary?.

Posted: Fri, 26 May 2023 07:00:00 GMT [source]

The Cheapest Places to Live in Los Angeles

An FHA loan is government-backed, insured by the Federal Housing Administration. FHA loans have looser requirements around credit scores and allow for low down payments. An FHA loan will come with mandatory mortgage insurance for the life of the loan. Your loan program can affect your interest rate and total monthly payments. Choose from 30-year fixed, 15-year fixed, and 5-year ARM loan scenarios in the calculator to see examples of how different loan terms mean different monthly payments. The mortgage payments assume a 20% down payment, and they include property taxes and home insurance.

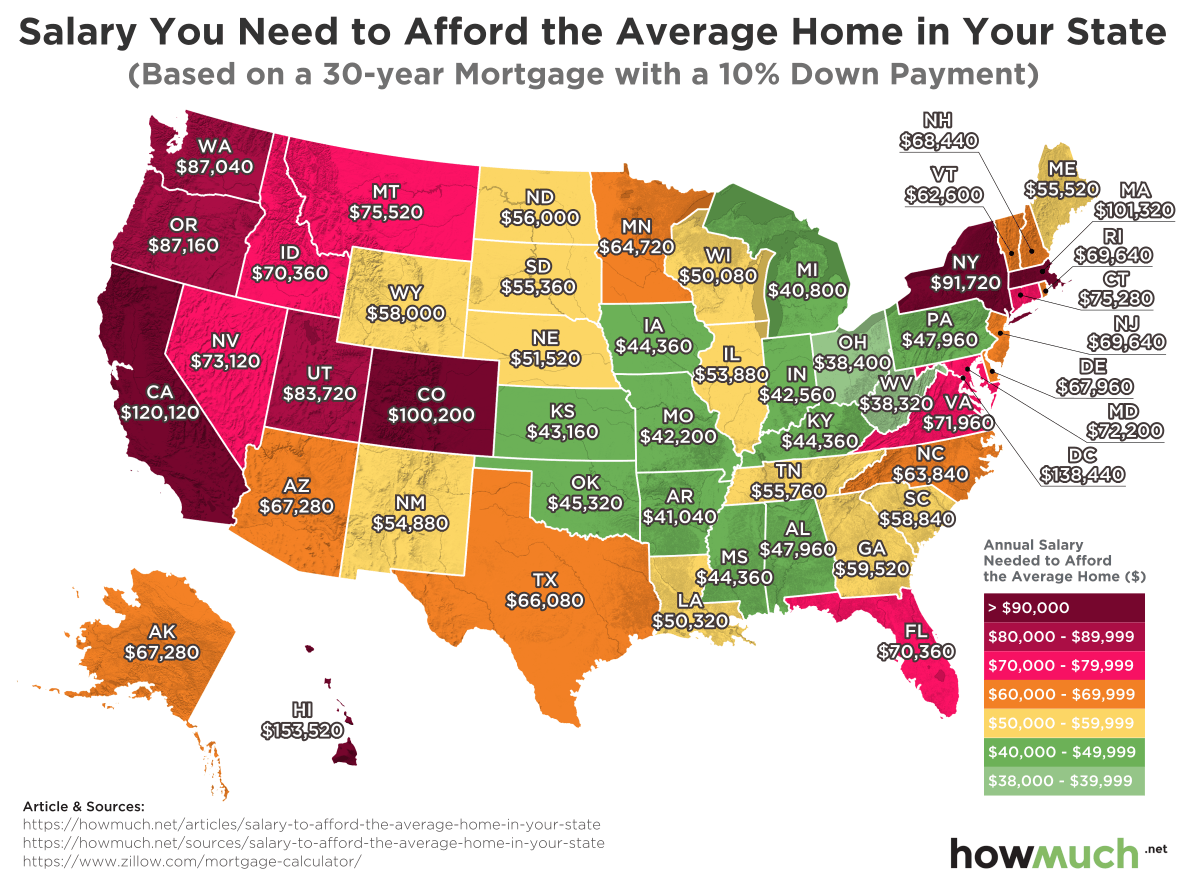

How Much House Can I Afford On A $120K Salary? - Bankrate.com

How Much House Can I Afford On A $120K Salary?.

Posted: Tue, 03 Oct 2023 07:00:00 GMT [source]

Mortgage Calculator

Two benefits to this mortgage loan type are stability and being able to calculate your total interest on your home upfront. Most banks don’t like to make loans to borrowers with higher than a 43% debt-to-income ratio. Although it’s possible to find lenders willing to do so (but often at higher interest rates), the thinking behind the rule is instructive. For decades, Dave Ramsey has told radio listeners that the best way to buy a house is paying for it in cash. As the cost of homebuying climbs, first-time buyers need a six-figure salary to purchase the average home. Research released Monday from real estate company Clever finds that with a 10% down payment, buyers need to earn nearly $120,000 to afford a median-priced home.

Use our mortgage calculator to determine your home budget.

When lenders evaluate your ability to afford a home, they take into account only your present outstanding debts. They do not take into consideration if you want to set aside $250 every month for your retirement or if you’re expecting a baby and want to save additional funds. The home affordability calculator provides you with an appropriate price range based on your input. Most importantly, it takes into account all of your monthly obligations to determine if a home could be comfortably within financial reach. That’s a big deal, because mortgages backed by the Department of Veterans Affairs typically don’t require a down payment.

When Kevin went to buy a 'few' model ships, he stumbled upon a lifetime collection

Be a more confident homebuyer with exclusive access to insights from a one-stop real estate tool for Wells Fargo customers. Get informed about the mortgage and homebuying process, from starting your home search to planning your next move. Budget 1% to 4% of your home’s value each year for home maintenance.

How much mortgage payment can I afford?

Your interest rate will affect both your monthly payment and your total home buying budget. Reserves refer to the number of monthly mortgage payments you could make from your savings if you lost your job or experienced another event that impacted your ability to make your payment. Every loan program is different, but a good guideline is to keep at least 2 months’ worth of mortgage payments in your savings account. Once you close on your home loan, your monthly mortgage payment may well be the biggest debt payment you make each month, so it’s important to make sure you can afford it. Your monthly payment and down payment are probably the two biggest factors in determining how much you can afford.

Your mortgage lender typically holds the money in the escrow account until those insurance and tax bills are due, and then pays them on your behalf. If your loan requires other types of insurance like private mortgage insurance (PMI) or homeowner's association dues (HOA), these premiums may also be included in your total mortgage payment. Most financial advisors agree that people should spend no more than 28 percent of their gross monthly income on housing expenses, and no more than 36 percent on total debt. The 28/36 percent rule is a tried-and-true home affordability rule of thumb that establishes a baseline for what you can afford to pay every month.

Homeowners insurance and property tax rates have been provided by Redfin, and are calculated at 0.22% and 1.25% a year respectively. This home affordability calculator provides a simple answer to the question, “How much house can I afford? ” But like any estimate, it’s based on some rounded numbers and rules of thumb. Here’s a look at the most common expenses to expect when buying a home and how you can translate your income and current debt load into a guideline for how much you can spend on a house. Add up your debt obligations such as car loans, credit cards, personal loans or other mortgages and enter the total.

What is Private Mortgage Insurance (PMI)?

This allows you to better compare how much mortgage you can afford from different lenders and to see which is the right one for you. Use the affordability calculator to see how your down payment affects your home affordability estimate and your monthly mortgage payment. That may also mean the cost of buying a home is at a historic high, although property buyers in the 1980s dealt with mortgage rates that were significantly higher than today's loans.

We’ll check your credit history to give you an even more solid estimate of what you can afford, along with your expected rate and monthly payment. Amy Fontinelle is a freelance writer, researcher and editor who brings a journalistic approach to personal finance content. Amy also has extensive experience editing academic papers and articles by professional economists, including eight years as the production manager of an economics journal. It only makes sense to make a large down payment if you have a lot of cash on hand and would like to avoid paying PMI or reduce your monthly payments. If making a large down payment would erase your financial reserves for future emergencies, then this is not a good idea. Once again, the answer to this question will depend on where you want to buy and what kind of property you want.

Take stock of your finances to see if you’re ready to apply for a mortgage. Make sure that you can provide evidence of at least two years’ worth of regular income, and figure out your total assets, debt and monthly expenses. If you wait, you may be able to get a better interest rate later, which could save you thousands of dollars in the long run.

No comments:

Post a Comment